At the present time, there is a surging need for making vehicles lightweight in order to increase their fuel efficiency. Because of this, there has been a shift in preference from traditional to new automotive assembly techniques. Conventionally, mechanical fasteners and welds, which provided increased strength and high performance, were utilized for bonding different parts of vehicles. However, now that the need for fuel-efficient vehicles had risen, manufacturers have started using lighter gauge metals, nonferrous metals, plastics, and coated steels for new vehicle designs. Attributed to this, the usage of holt melt adhesives for joining different automobile parts is rising.

Get the Sample Copy of this Report @ https://www.psmarketresearch.com/market-analysis/hot-melt-adhesives-market/report-sample

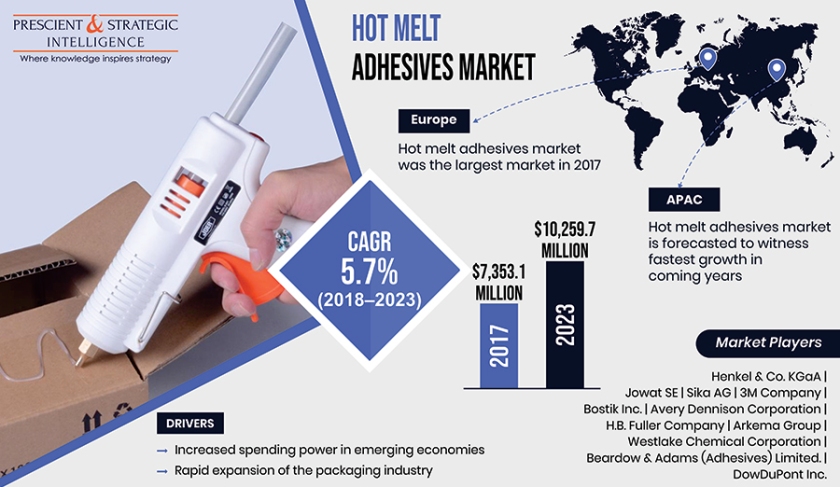

Hot melt adhesives, also known as hot glue, are thermoplastic adhesives applied using a hot glue gun. As per a report by P&S Intelligence, in 2017, the global hot melt adhesives market generated a revenue of $7,353.1 million and is projected to attain a value of $10,259.7 million in 2023, witnessing a 5.7% CAGR during the forecast period (2018–2023). Among all the regions, namely Asia-Pacific (APAC), Europe, North America, and Rest of the World, Europe created the largest demand for hot melt adhesives during 2013–2017; however, during 2022–2023, the APAC region is expected to create the highest requirement for these adhesives.

The different product types of hot melt adhesives are styrenic block copolymer (SBC), polyamide (PA), metallocene polyolefins (MPO), ethylene vinyl acetate (EVA), polyurethane (PU), amorphous polyalphaolefins (APAO), and polyester. The EVA category was the largest in demand during 2013–2017 and is further predicted to retain its position during the forecast period. This is attributed to the different advantages of this product, such as long shelf life, quicker setting time, and suitability in a range of temperatures. In addition, the expansion of the construction and automobile industries is also creating increasing demand for EVA. The fastest growth in demand is projected to be witnessed by the PU category in the coming years.

Make Enquiry Before Purchase @ https://www.psmarketresearch.com/send-enquiry?enquiry-url=hot-melt-adhesives-market

When application is taken into consideration, the hot melt adhesives market is divided into diapers, footwear, automobile, bookbinding, packaging products, furniture, textile, electronics, and others (which include filter and floristry industry). Out of these, the largest demand for hot melt adhesives was created for the packaging products application during 2013–2017 and situation is expected to remain the same in the near future as well. The fastest growth in demand is predicted to be registered by the furniture application in the coming years, owing to the growing need for fulfilling the demand of the rising population in countries including Germany, China, and India.

The rapid expansion of the packaging industry, which is occurring due to swift industrialization, is a key factor driving the requirement for hot melt adhesives. The rising purchasing power of individuals and changing consumption trend have resulted in the development of varied and eco-friendly products. The developing countries, primarily, are extensively making use of hot melt adhesives in packaging and automotive industries. The growing spending power in countries including Indonesia, China, and India has led to an increase in demand for various products such as electronics, clothes, and footwear, all of which use hot melt adhesives in different applications.